PagerDuty: Pioneering Digital Operations Management

Investment Thesis: Digital transformation has seen rapid acceleration across all industries as the pandemic forces remote work. As companies continue their digital transformation journey, they will need a digital operations management platform to manage all of their digital touchpoints to provide a frictionless end-user experience. PagerDuty's (PD) platform enables companies to proactively manage their entire digital infrastructure from incident response to business analytics. With limited competition in a rapidly growing space, PagerDuty could see substantial upside over the next few years.

Digital Transformation

Cloud Adoption

The IDG 2020 Cloud Computing Survey surveyed 551 IT professionals and reported that 43% described their IT environment to be mostly cloud and some on-premise while 16% described their IT environment to be all cloud in the next 18 months. IDG also reported 32% of total IT budgets will be allocated to cloud computing over the next year.

In addition to cloud adoption for companies, more individuals and devices are being connected to the internet every day (check out the statistics in my previous article). This means companies will need to focus on providing frictionless digital experiences for end-users to remain competitive.

Digital Maturity and Financial Performance

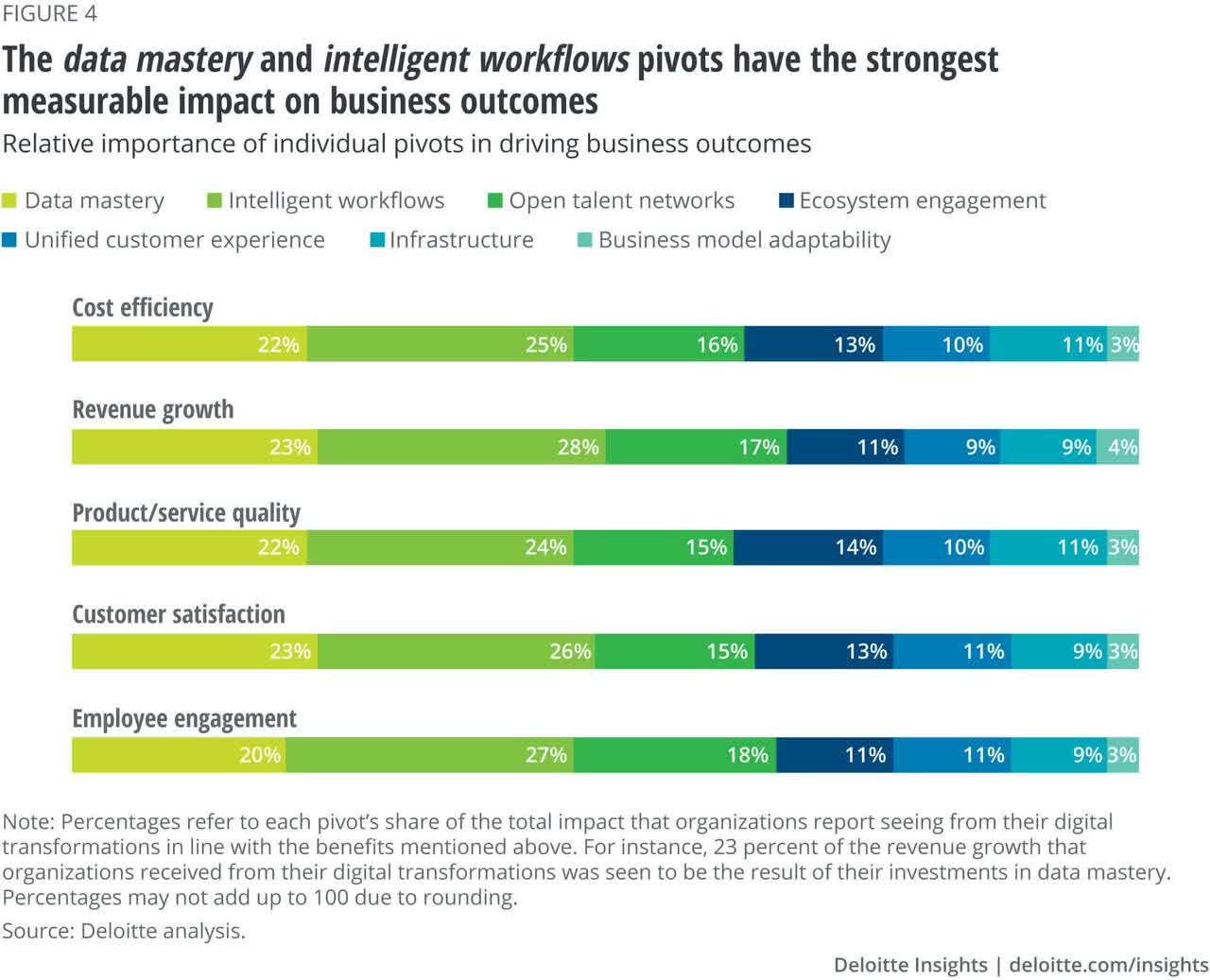

There are proven financial benefits for companies who chose to invest in digital transformation and are more digitally mature than their competitors. An article by Deloitte describes 7 digital pivots that propel an organization towards digital maturity. Each of these pivots plays a part in digital operations management.

Investment in these digital pivots to improve financial performance relative to those who are less digitally mature. Deloitte states that companies with higher digital maturity reported revenue growth of 45% and net profit margin of 43% whereas companies with lower maturity reported revenue growth and net profit margin of 15%.

Better financial performance with regards to revenue growth and profit margins is because companies with higher digital maturity gain insights to improve product/service quality, customer satisfaction, employee engagement, and focus more on growth and innovation as opposed to costs reduction.

Data mastery and intelligence workflows are seen as having the largest impact on business performance based on Deloitte's findings. This shows the importance of proper data utilization and AI/ML in a company's operations.

Revenue will be more dependent on digital means than traditional means as more industries continue to offer digital services. In fact, a survey by Workday revealed that over one-third of firms expect 75% of revenue to come from digital in the next 3 years. The number has tripled since the same survey in 2019. If end-users experience issues with a digital touchpoint with one company, the switching costs to use a competitor's digital service are typically low.

To ensure companies seamlessly transition to a digital infrastructure, they will require a digital operations platform that monitors all business functions and provides teams with insights into possible incidents that may affect business performance.

PagerDuty

PagerDuty provides a real-time operations platform that implements machine learning to process digital signals created by any software-enabled device and alerts the correct team members to take action. These digital signals act as indicators of events that may affect customer experience or business operations. The platform was initially created to provide an on-call management service, then added functionality for incident management, and has recently made an acquisition to extend into AIOps (artificial intelligence for IT operations) and extend its position as a leading digital operations management platform.

Business Model

PagerDuty’s platform provides the following products:

On-Call Management: This was the foundation of PagerDuty when it was founded in 2009. This service allows aids companies with orchestrating a coordinated response by automating the process of identifying, triaging, and managing incidents. Features include live call routing, scheduling, incident management, dynamic notifications, and automated escalations. PagerDuty provides mobile support for on-call management on iOS and Android enabled devices.

Modern Incident Response: This is an extension of on-call management. Modern Incident Response includes automation of workflows and engagement of cross-functional teams to allow for a rapid response. Modern Incident Response integrates with ITSM tools like ServiceNow which automate the ticketing process for customer service requests.

Event Intelligence: The company states their Event Intelligence product applies ML to correlate and automate the identification of incidents from billions of events. As the PagerDuty platform integrates with other services, Event Intelligence allows for the grouping of related incidents into a single event and distinguishes between actionable and non-actionable events while continuously learning allowing teams to be more productive.

Visibility: This product provides different departments of a business a shared, holistic view into the real-time operational health and quantifies the business impact as an incident is occurring.

Analytics: Helps business leaders to understand the impact of operations. It combines data with business metrics to provide insights into the digital operations performance, impact on customers and employees, and cost to the business.

A key feature of the platform is its ability to integrate with over 500 over the most popular applications, APM environments, security and threat management systems, ticketing systems, etc. Some names include AWS, ServiceNow, Datadog, Zendesk, Slack, and Cloudflare. This allows PagerDuty to act as "the central nervous system of the digital enterprise". PagerDuty integrates with all these services and aggregates digital signals from each one to orchestrate a real-time response across different teams.

PagerDuty's pricing model is based on a per user per month basis. Many customers enter into agreements for yearly contracts but some customers maintain a month-to-month pricing structure. The company recently adopted a freemium approach as well.

Growth Areas

Upselling within existing customer base: In the most recent 10-K, PagerDuty mentions that on-call management derives a substantial portion of their revenue. This is seen as a major risk due to high revenue concentration but also has a source of growth for expansion to use cases outside of on-call management.

Recent earnings calls have mentioned new customers adopting across all business units including legal to manage real-time workflows. As businesses continue adopting this across different functional departments I expect other products (Analytics, Visibility, Event Intelligence) to be a larger driver in revenue growth.

Expanding uses cases: PagerDuty describes its platform as horizontal meaning it can be applied to verticals outside of just developers and ITOps. The company needs to continue bringing to market products that can benefit these verticals as they did with Analytics and Visibility. This will be critical for driving DBNRR, revenue growth, and diversifying revenue concentration.

PagerDuty leverages a land-and-expand business model with a focus on a self-service model. This enables teams to get started without any assistance.

To upsell and cross-sell more effectively PagerDuty uses a mix of field and inside sales teams. Sales and Marketing is expected to be the largest expense for the foreseeable future as it is a major contributor to revenue and customer growth.

Expanding use cases will also be crucial to deepening their competitive moat. As PagerDuty becomes more integrated into a company's infrastructure, switching costs increase.

In an effort to continue expanding use cases, PagerDuty recently acquired Rundeck. Rundeck allows incident response teams to implement automated workflows to increase productivity and recovery efforts.

International Expansion: Growth in international revenue has been impressive with 36% YoY in the most recent quarter. However, international revenue accounts for roughly 23% of total revenue. Management has mentioned large healthcare enterprises and even major banks abroad adopting PagerDuty's solution across their infrastructures. I expect international revenue to become a larger portion of total revenue as PagerDuty continues to strengthen its position as the leading digital operations platform globally.

PagerDuty states a TAM of $100 billion including both incident management and digital operations management as a whole. This is based on PagerDuty's pricing structure and their estimate of the total potential users of their product. Management assumptions are typically overly optimistic but even with a TAM of a quarter of the size ($25 billion), there is a long runway ahead of the company which currently sits on a market cap of $3.8 billion.

Moat

Switching Costs

PagerDuty's platform creates switching costs in two ways. The first is through expanding use cases. As PagerDuty expands the functionality of its platform, companies can integrate PagerDuty into more business units, which makes the company more reliant on the platform leading to higher switching costs.

PagerDuty builds on these switching costs through its Modern Incident Response product. When a company utilizes the incident response solution, it begins to continuously learn from the actionable and non-actionable events and begins to provide preventative solutions instead of reactive ones over time. For this reason, I think it's critical for PagerDuty to change their pricing to a per-user per-year basis as it forces customers to keep PagerDuty's services longer, giving customers time to experience the full capabilities of the platform which will lead to higher switching costs. The graphic below describes the transition from reactive solutions to preventative ones as companies' digital operations mature.

The power of switching costs is typically measured by a company's ability to upsell or cross-sell to an existing customer base, or DBNRR. PagerDuty reported a DBNRR of 119% in the most recent quarter and 122% for FY20. The median DBNRR for the top SaaS companies is 119% based on data from Atom.

Financials

PagerDuty has seen slowed growth since the pandemic but has improved gross margins to 86% and maintained revenue growth of 26% in the most recent quarter. Billings for the quarter are up 26% YoY and were up 36% YoY in FY20. Billings growth for NME FY21 was 22% which is still impressive given pandemic headwinds.

The company has yet to turn a profit with operating expenses representing 126% of revenue and an operating margin of -40% in the most recent quarter. This increase in operating expenses was primarily due to sales and marketing which were higher than normal in Q3 due to headcount growth. Operating loss for NME FY21 is $47m compared to $43m over the same period in FY20. The company's operating margins have improved from -48% in FY18 up to -33% in FY20 but still far from profitability.

Free cash flow for the most recent quarter was $5m representing FCF margin of 8%. FCF for NME FY21 is only $3m representing a 2% FCF margin. However, SBC has been a significant contributor to cash flow from operations. Excluding SCB, FCF for the same period is -$28m representing a FCF margin of -18%.

Company-Specific Metrics

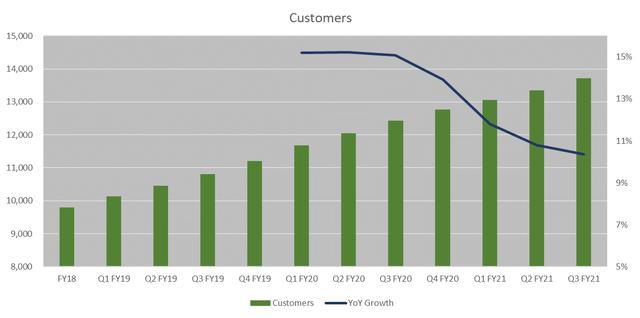

PagerDuty has managed to continue expanding its customer base to 13,725 with a 10% YoY increase in the most recent quarter. The number of customers with ARR greater than $100,000 has reached 401 representing an increase of 32% YoY. Growth in customer base has slowed since the end of FY20, however, I think this is largely due to pandemic headwinds and companies focused on cost-cutting.

DBNRR has been in a downtrend since the end of FY19 where it peaked at 140%. The company reported 119% DBNRR in the most recent quarter which is still impressive. However, given the increased sales and marketing expense and lowering DBNRR it seems as if the company has an inefficient sales strategy.

Overall PagerDuty's financial performance is subpar. There has been some stagnation in growth revenue, customers, lower DBNRR, and deeper operating losses in the most recent quarter. This may due to headwinds from the pandemic but time will tell. Nevertheless, the company doesn't need to worry about any debt obligations with cash and short-term investments of $556m compared to total liabilities of $403m.

Competitive Landscape

xMatters is a privately-held pure-play competitor to PagerDuty. Based on data from PrivCo, xMatter is smaller than PagerDuty and lacks revenue growth with $42.1m in revenue in 2019 compared to $39m in 2016. The company was valued at $150m in February 2018 in its last funding round. xMatters offers integrations to cloud monitoring and APMs similar to PagerDuty but only offers 123 integrations compared to PagerDuty's over 500 integrations with the acquisition of Rundeck. The platform offers all the same features as PagerDuty including automation of business processes but doesn't clearly state if their products implement ML the same way PagerDuty's Modern Incident Response product does. However, I'd assume they do.

Other competitors include OpsGenie (TEAM), and VictorOps (SPLK). OpsGenie and VictorOps are products apart of a larger portfolio of products for their respective companies. Additionally, based on reviews its seems that OpsGenie and VictorOps aren't as appealing and are less popular. Both companies offer incident management solutions but don't seem to extend functionality beyond on-call management and incident response. Here's an overview of each company's financial performance over the past 3 years:

Valuation

Since there are not any publicly traded, pure-play competitors to PagerDuty but I will use TEAM and SPLK as comparables. This is not an apples to apples comparison given the size difference between PagerDuty, TEAM and SPLK. As seen above, PagerDuty maintains higher revenue growth and gross margins than both TEAM and SPLK but is significantly smaller with annual revenue of only $166m compared to TEAM and SPLK who reported $1.6bln and $2.4bln, respectively.

PagerDuty has the highest consensus revenue growth for the next year and maintains higher gross margins but is only trading at a 13x forward TEV/Revenue compared to TEAM's 28x forward TEV/Revenue multiple. Also important to note PagerDuty suffered significant operating losses in the most recent fiscal year.

I think PagerDuty may be slightly undervalued based on this comparison, however, there are several risk factors to consider that may justify its lower valuation. However, I remain cautiously bullish at these prices due to future growth prospects and limited competition.

Risks

Revenue concentration: PagerDuty mentioned that on-call management accounts for a substantial amount of total revenue for the company. There are plenty of alternatives for on-call management platforms therefore it is critical for the company to up-sell customers to other products (incident response, analytics, etc.) which will also result in higher switching costs for customers.

Ineffective sales strategy: As mentioned above, the company has seen higher sales and marketing expenses due to an increase in the number of employees but has seen slowed growth in customers and a consistently lower DBNRR.

This can be due to companies focused on cost-cutting during the pandemic or due to PagerDuty's sales strategy being ineffective. If the former is the case, I don't this as a long-term headwind. However, if PagerDuty's sales strategy is ineffective it can be detrimental to the future growth prospects of the company.

Failure to expand use cases: In order to continue upselling to new and existing customers, PagerDuty will need to continue innovating and extending the functionality of its platform beyond just on-call management and incident response.

Other incident management platforms lack the number of integrations compared to PagerDuty and don't extend the functionality beyond incident response. Expanding use cases serves as a differentiating factor and strengthens their competitive moat. Failure to do this will result in a deteriorating moat.

Conclusion

The rapid digitization of enterprise infrastructures and operations has resulted in increased demand for digital operations management. PagerDuty offers a platform that extends beyond on-call management and incident response and continues to expand beyond use cases for strictly ITOps and developers. The company faces little competition from its existing competitors but has seen slowed growth and deeper operating losses over the past two quarters.

If this due to headwinds from the pandemic, I think the company still has significant upside as companies continue focusing on digital transformation in the future. However, if the company continues to perform poorly post-pandemic I'll be worried. Until then I remain cautiously bullish and will monitor DBNRR, operating margins, and revenue growth closely in future earnings reports to see if my thesis holds.