Fiverr: Q4 FY20 Update

Before reading this checkout my initial FVRR coverage here. This post will be an extension of what I previously covered with some additional areas I failed to cover initially. Subscribe to stay up-to-date with my latest posts.

Update on Investment Thesis: Remains largely the same. However, critical factors to watch going forward include their e-learning platform, additional “back office” services for freelancers, and additions to Fiverr Business. Expanding services offered to users of their platform outside of just buying and selling gigs will be crucial to embedding switching costs for all users.

The Freelance Economy

Some highlights on the freelance economy from my previous report:

Freelancers earned $1.2T, a 22% increase YoY, in 2020 representing 5% of US GDP.

36% of the American workforce freelanced in 2020 representing 59MM people vs 57MM in 2019.

The number of full-time freelancers and freelancers who freelance to supplement their income has increased 11% and 6%, respectively, and the number of part-time freelancers has dropped 15% since 2014.

Based on a McKinsey & Co survey from 2016, 150MM people provide labor as a service yet only 9MM (6%) provide their services through digital platforms.

The Future of the Workforce

“Eventually, super high-quality work will be available in a gig fashion.”

I recently listened to Naval Ravikant’s interview with Joe Rogan. (I highly recommend everyone to watch the full interview.) In the segment above, Naval discusses the future of the workforce and how the information age will reverse the industrial age resulting in everyone working for themselves. Albeit it sounds far-fetched, but it’s an emerging trend we are just beginning to see in the freelancing economy.

Naval discusses how hierarchies were formed as a result of the industrial revolution and prior to the revolution, going back to hunter-gather days, people for the most part worked for themselves. As people began working in factories, they become more accustomed to the idea of working for someone else and being subject to this hierarchical model.

He goes on to discuss why companies are the size they are. The reason has to do with the internal versus external transaction costs for a company. For example, if it’s cheaper to conduct a transaction internally than externally, a company will integrate that internally into their business. However, the information age is reducing the costs of external transactions making it more efficient to transact externally (ie. hiring freelancers through your smartphone). Obviously, all parts of a company can’t be outsourced, such as executive-level roles, however, this transition has begun at the lowest level of the hierarchy and will eventually lead to people working for themselves or at least in much smaller groups.

Additionally, as advancements in AI/ML continue to automate traditional human work, it will drive the need for creativity in the workforce which isn’t something AI will be replacing anytime soon. As a result, I expect the workforce to be centered around more creative work in the future.

This idea is just hypothetical but still something to consider. This idea of the future of the workforce looks even more promising when you look at the next generation of the workforce, Gen Z. Gen Zers are the first digitally native generation who grew up immersed in a world of Tik Tok and Instagram where they are forced to be creative. In fact, Adobe found that this generation is more creative than any previous generation.

Growth Drivers

I previously discussed the macro trends within the gig economy and the potential for continued growth in the future. But what’s fueling the growth in freelancers and the demand for freelancers?

Gen Z

Based on data from Upwork’s Freelance Forward report, the U.S. freelance workforce is becoming younger with 50% of Gen Z and 44% of Millennials participating in freelance work in 2020. Of those that began freelancing for the first time in 2020, 57% were Millennials while only 12% of Gen Z fit this criterion. Millennials are already in the workforce whereas Gen Zers are just beginning to enter the workforce.

Gen Z represents a cohort of individuals born between 1997-2012. Gen Z is currently the largest cohort alive with nearly 2 billion people globally, representing 26% of the world’s population. The youngest individuals in the cohort are expected to enter the workforce in 2040 (given workforce includes those over 18 years old). This will fuel the number of freelancers for years to come.

According to Upwork’s study, 90% of Gen Z freelancers are likely to do freelance work in the future and 71% of Gen Z freelancers started freelancing by choice over necessity. Of the Gen Z individuals who are not freelancers, 73% are likely to consider doing freelance work in the future.

Demand for Gig Platforms

Only 26% of skilled freelancers and 25% of new freelancers have found work through general freelance websites since the onset of the pandemic. Fiverr’s CEO Micha Kaufman stated their largest competitor is the offline market and these numbers show just that. This demonstrates a long runway for gig platform providers as well.

Demand for Freelancers

Freelancing has become increasingly more popular for freelancers for reasons which include autonomy, flexibility, better pay for skilled freelancers, and better work-life balance. Buyers of these services (individuals, SMBs, corporations, etc) also benefit from hiring freelancers. These benefits include cost-effectiveness and access to a wide variety of talent with specialty services.

For companies, hiring freelancers results in less commercial real estate, cheaper pay for companies located in major cities, less training required for skilled freelancers, and the ability to scale the workforce easily all of which lead to cost savings. Based on current legislation, companies aren’t required to provide benefits for freelancers as they would to traditional employees which also helps cut costs. This may change in the future.

Fiverr

Business Model

Refer back to my previous report. Here’s a high-level overview:

Moat

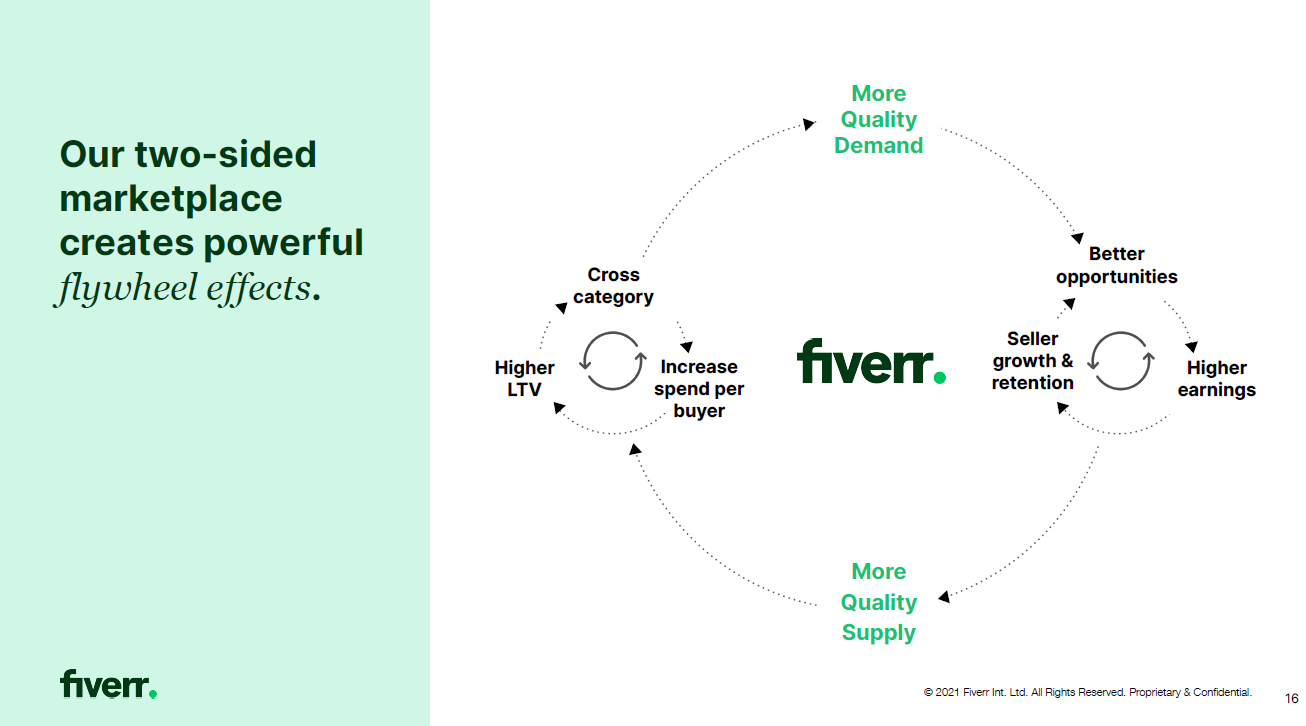

In my previous report, I incorrectly interpreted the network effects for Fiverr. I discussed counter positioning and how that creates a moat against incumbents but failed to classify the flywheel effect as a network effect.

Fiverr’s network effect comes from its freelancers providing higher-quality services which results in higher-quality demand. As the quality of services provided begins to improve, Fiverr can continue to sell upmarket resulting in higher average transaction size and more incentive for freelancers to provide higher-quality services. This creates a positive feedback loop as seen in the graphic below:

I also previously discussed the network effects that arise from Fiverr’s ML algorithm that personalizes suggestions for buyers, however, these network effects don’t create any significant competitive advantage as it can be easily replicated by any competitor. Nevertheless, Fiverr’s ability to personalize suggestions to buyers does enhance cross-selling between categories and LTV of buyers.

Material Developments

Working Not Working Acquisition

Fiverr recently announced the acquisition of Working Not Working, a platform for high-end creative talent. Fiverr states the goal of this acquisition is to improve their catalog infrastructure with higher quality freelancers in the creative space. Working Not Working helps top creative talent connect with major brands (Google, Nike, American Express, etc.) around the world. The quality of talent is much better than what Fiverr currently offers and will be important to their strategy of selling upmarket. Exactly how this acquisition will play out isn’t clear but Fiverr plans to leverage their technology with Working Not Working’s creative talent and SLT Consulting’s services, a digital marketing consulting firm, to create products that benefit the marketing and advertising communities.

Fiverr acquired Working Not Working for $9.4 million in cash with an additional $3.5 million payments contingent on certain milestones to be paid over a three-year period. Working Not Working will continue to operate as a standalone entity.

Update on Growth Drivers

International Expansion: Fiverr emphasized its efforts to expand internationally. The company has built a linguist team to help with the localization of Fiverr’s website. This localization strategy has already been implemented in Germany and Fiverr has seen higher conversion rates on the localized websites compared to the English-only website. Currently, Fiverr offers six non-English languages.

Fiverr states majority of its core marketplace revenue comes from Gigs purchased by buyers located in the US, UK, Canada, Australia, and New Zealand. Fiverr expects to continue expanding internationally and introduce localized websites for countries in Western Europe, Asia Pacific, and Latin America.

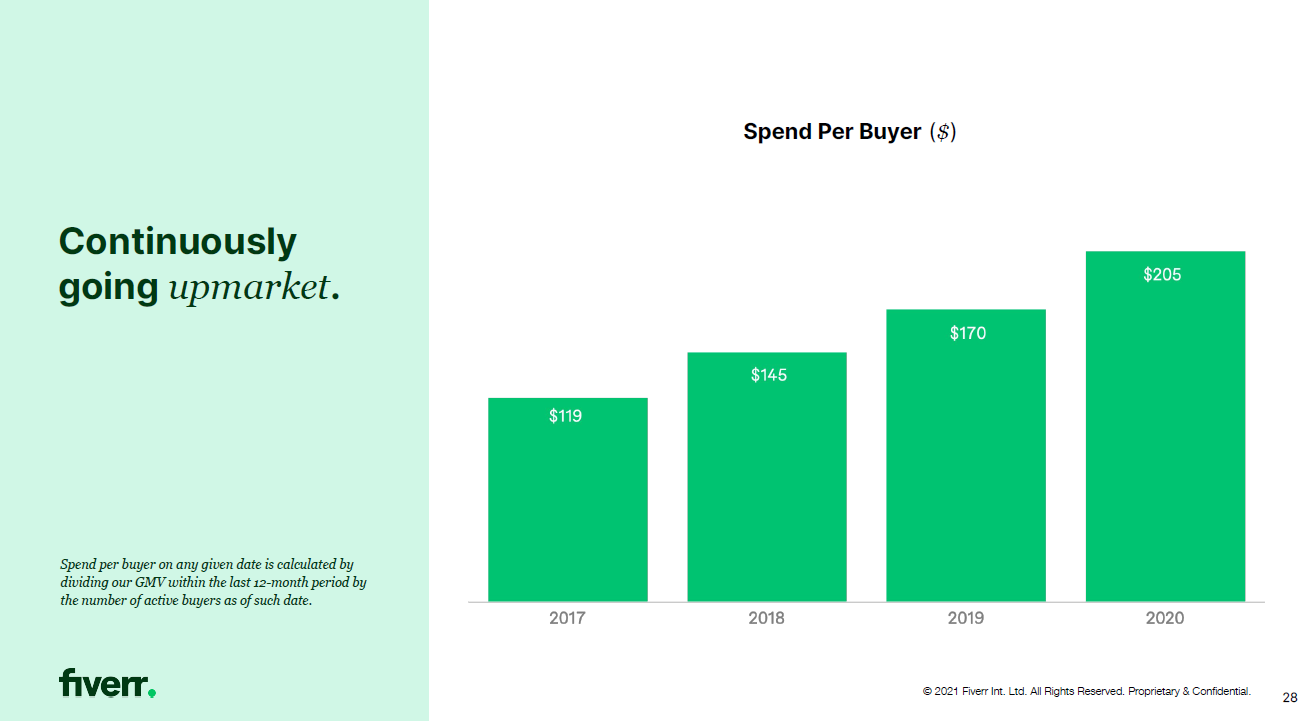

Selling Upmarket: Fiverr’s GTM strategy to start small and eventually pursue selling upmarket has been successful thus far as measured by spend per buyer. Spend per buyer for FY20 was $205 (+21% YoY) and has seen consistent growth since FY17.

Source: Fiverr Investor Presentation Category Expansion: Fiverr has continued to add approximately 30 new categories per quarter. Currently, Fiverr offers 500+ categories for digital services.

Critical Factors

As competition in the gig platform space intensifies, it will be important for Fiverr to deepen its moat by creating switching costs for freelancers. The following critical factors will be crucial for Fiverr to deepen its moat:

Fiverr Learn: Fiverr Learn is an online learning platform where people can purchase courses for a fixed price. Fiverr has expanded its course selection in recent months to cover seven different categories. The video lectures seem to be of high quality and taught by industry experts. Fiverr’s ability to continue to expand its course offerings will allow freelancers to improve their skills, provide higher quality services, and perpetuate the flywheel effect.

Currently, the pricing structure for Fiverr Learn is a pay-per-course model. However, it would be interesting to see Fiverr partner with Skillshare or Udemy to provide a much larger set of educational content through a subscription service.

An end-to-end platform: Fiverr’s acquisitions of And.Co and ClearVoice have allowed them to offer back-office services to freelancers other platforms don’t offer. And.Co provides a business management software that helps entrepreneurs manage their invoices, projects, proposals, contracts, and income/expenses. ClearVoice helps entrepreneurs with content creation and marketing. For buyers, Fiverr introduced Fiverr Business which allows for businesses to better manage their freelancers and project workflow.

And.Co and ClearVoice are provided to freelancers through their own respective websites but incorporating them into Fiverr’s seller dashboard would be a step toward creating a one-stop-shop freelancing platform. Fiverr’s ability to embed switching costs for both freelancers and buyers into their platform is what will determine their long-term success.

Financial Performance

Highlights (FY20 vs FY19)

GMV: $700MM (+74%) vs. $401MM (+37%)

Revenue: $189MM (+77%) vs. $107MM (+42%)

Based on guidance, revenue growth for FY21 is expected to be $277MM - $284MM (+46-50% YoY)

Management did state the guidance is conservative and does not take into consideration additional products and features expected to be launched this year.

Fiverr derives 73% of its revenue from transactional fees and 27% of additional services which include Fiverr Learn, And.Co, ClearVoice, and Fiverr Business.

Gross margin: 83% vs 79%

Operating margin: -6% ($-$12MM) vs. -33% (-$35MM)

Adj. EBITDA margin: 4.8% ($9.1MM) vs. -16.8% (-$18MM)

CFO margin: 9% (17MM) vs. -13% (-$14MM)

FCF margin: 8% ($15MM) vs.-14% (-$15MM)

Sales & Marketing

Sales and marketing continue to be Fiverr’s largest operating expense as a percent of revenue even though the company states it doesn’t have a direct sales team. Instead, Fiverr focuses on performance marketing and measures its efficiency of this strategy using a metric called “Time to Return on Investment” (tROI). tROI represents the number of months it takes to recover performance marketing investments from revenue generated by new buyers. Fiverr targets a tROI of fewer than 1 year but has managed to achieve a tROI of fewer than six months for the last two years. Here’s a breakdown of tROI by buyer cohort:

Company-Specific Metrics (FY20 vs FY19)

Take Rate: 27.1% vs. 26.7%

Note: 25% of take rate is transactional (20% from sellers + 5% from buyers). Any excess is generated from ancillary services such as Fiverr Learn, And.Co, ClearVoice, Promoted Gigs, and Fiverr Business. Growth in the take rate indicates freelancer adoption of these additional services which can increase the stickiness of the platform creating switching costs for users.

Active Buyers: 3.4MM (+45%) vs. 2.4MM (+16.5%)

Spend per buyer: $205 (+21%) vs. $170 (+17.2%)

Repeat Buyers as % of Revenue: 55% vs 58%

This decrease in repeat buyers was due to the influx of new users during the pandemic. This is an important metric to watch as a way to monitor platform stickiness.

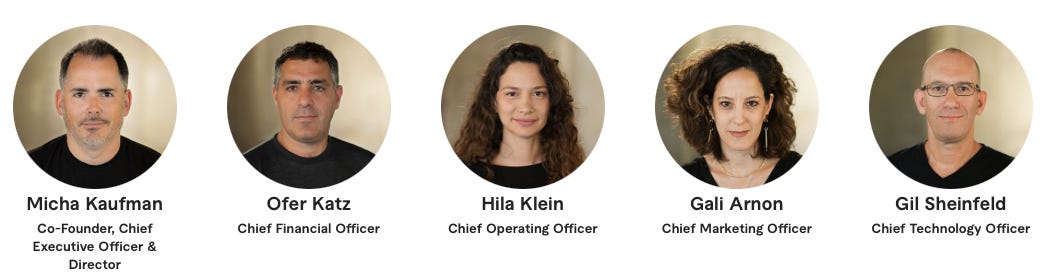

Management

Fiverr was founded by Micha Kaufman and Shai Wininger in 2010. Kaufman serves as the CEO of Fiverr and Wininger left Fiverr in 2015 to start Lemonade, a tech-enabled insurance company. Kaufman and Wininger still have significant ownership with each owning 5.45% and 4.79%, respectively. Here’s a breakdown of Fiverr’s ownership:

Fiverr is based in Israel and is backed by a management team composed of a group of highly-experienced executives. Both Kaufman and CFO Ofer Katz have had led multiple start-ups in the past and have continued to execute on their vision of Fiverr they set out at its inception. Kaufman mentioned the initial goal of Fiverr was to provide $5 gigs for buyers, hence the name “Fiverr”, and eventually expand upmarket and provide higher-quality services for larger buyers. Thus far, Fiverr has done a phenomenal job executing this plan.

Fiverr’s GlassDoor reviews are excellent with a 96% approval of CEO and 4.5/5 star rating.

Here’s a podcast with Micha Kaufman where he discusses why he decided to start Fiverr, his experience building the company, and what he wants Fiverr to become.

Competitive Landscape

Upwork

Upwork originally began providing enterprises with skilled freelancers and was seen as a traditional staffing company. However, recently Upwork launched its Project Catalog service which directly competes with Fiverr in an effort to deviate from being seen as strictly a staffing company. Upwork following in Fiverr’s footsteps demonstrates that the future of work is centered around the gig economy. With this new service, Upwork’s and Fiverr’s target markets begin to converge which will intensify the competition between the two leaders in the space.

Upwork’s Project Catalog page is almost identical to Fiverr’s website. This makes it seem as if Upwork launched this service as quickly as possible without any original thought. Additionally, the process of creating a client account versus a freelancer account is a bit tedious. Upwork makes users create two individual accounts to act as a client and a seller. As I tried to sign up for both, I ran into the problem of not being able to use my phone number for my freelancer account because it had already been linked to my client account. This could be a flaw on my end but I tried every solution I could find and still no luck. Furthermore, Upwork also requires users to download separate mobile apps for freelancer accounts and client accounts creating more friction between switching accounts.

Upwork lacks the additional features Fiverr provides through Fiverr Learn, Fiverr Pro, Fiverr Business, Fiverr Logo Maker, Fiverr Studios, And.Co, and ClearVoice. Fiverr has the first-mover advantage in the space which has helped them build strong brand recognition. However, both platforms lack any significant switching costs for both freelancers and buyers. It will be important going forward for Fiverr to continue adding features that embed switching costs, for both freelancers and buyers, into their platform.

Financials (FY20 vs FY19)

GMV: $2,500MM (+21%) vs. $2,100MM (+19%)

Revenue: $374MM (+24%) vs. $301MM (+42%)

Gross margin: 72% vs 71%

Operating margin: 6% (-$22MM) vs. -6% (-$19MM)

Adj. EBITDA margin: 4% ($14MM) vs. 2% ($7MM)

CFO margin: 6% (22MM) vs. 0.5% ($1MM)

FCF margin: 4% ($16MM) vs. -3% (-$10MM)

Company-Specific Metrics

Take Rate: 13.6% vs. 13.1%

Core Clients: 145K (+17%) vs. 124K (+19%)

(Important note: "Core Clients" only represents clients who have spent at least $5,000 since the first purchase and have had spend activity in the past 12 months. Fiverr's "active buyers" represents anyone who has ordered a gig within the last 12 months.)

Client Spend Retention: 102% vs 102%

Fiverr charges a significantly higher fee (25%) for both buyers and freelancers compared to Upwork. Upwork charges a “sliding fee” where the percentage decreases as lifetime billings per client increases. For example, for the first $500 billed with a client Upwork takes 20%, between $500 - $10,000 Upwork takes 10%, and anything more than $10,000 Upwork takes 5%. For buyers, Upwork charges a 3% processing fee.

The primary reason I think Fiverr is able to charge a higher fee is because of the additional value the platform provides for both freelancers and buyers compared to its competitors. This higher take rate can be a risk to Fiverr if competing platforms begin offering similar services to Fiverr or if the quality of Fiverr’s services deteriorates.

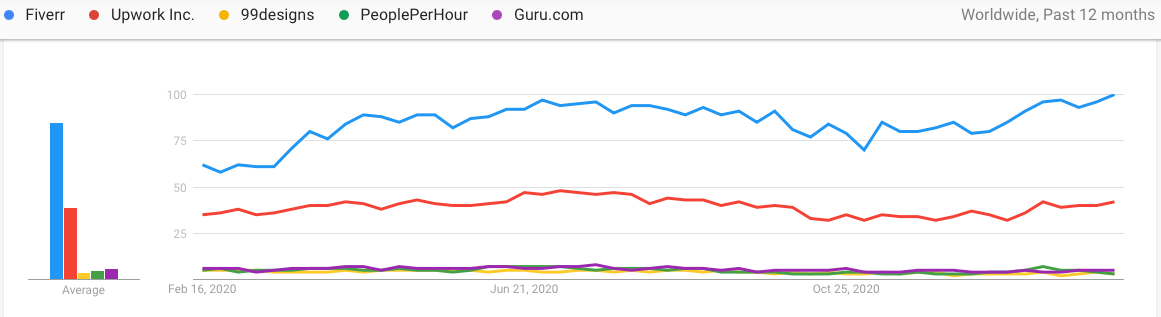

Worldwide Search Interest

Below is a chart showing worldwide search interest for Fiverr, Upwork, 99designs, PeoplePerHours, and Guru.com. Fiverr’s search interest is at all-time highs relative to its competitors.

Mobile App Ratings

Other Competitors

LinkedIn Freelance Marketplace

Microsoft recently announced they are planning to enter into the freelance space by providing a freelance marketplace service on LinkedIn. I think this could be Fiverr’s biggest competitive threat next to the offline market. LinkedIn has over 760 million users and 260 million monthly active users. LinkedIn is used by professionals to network and companies to post jobs. Incorporating a freelance marketplace within LinkedIn feels like it would be a perfect fit for the platform. Additionally, LinkedIn’s users consist of primarily white-collar professionals who are able to provide the same high-quality work Fiverr is attempting to provide for its users as it continues to sell upmarket.

Another competitive feature LinkedIn already has in place is LinkedIn Learning. This service is similar to what Fiverr is trying to do with Fiverr Learn but with a much larger selection of over 16,000 courses.

LinkedIn’s new service isn’t expected to launch until September 2021. It will be important to see how LinkedIn incorporates services from Microsoft like Teams, file sharing, cloud storage, etc. into the platform, in an effort to embed some sort of switching costs or platform stickiness, as well as how appealing LinkedIn’s service will be for creative talent.

Valuation

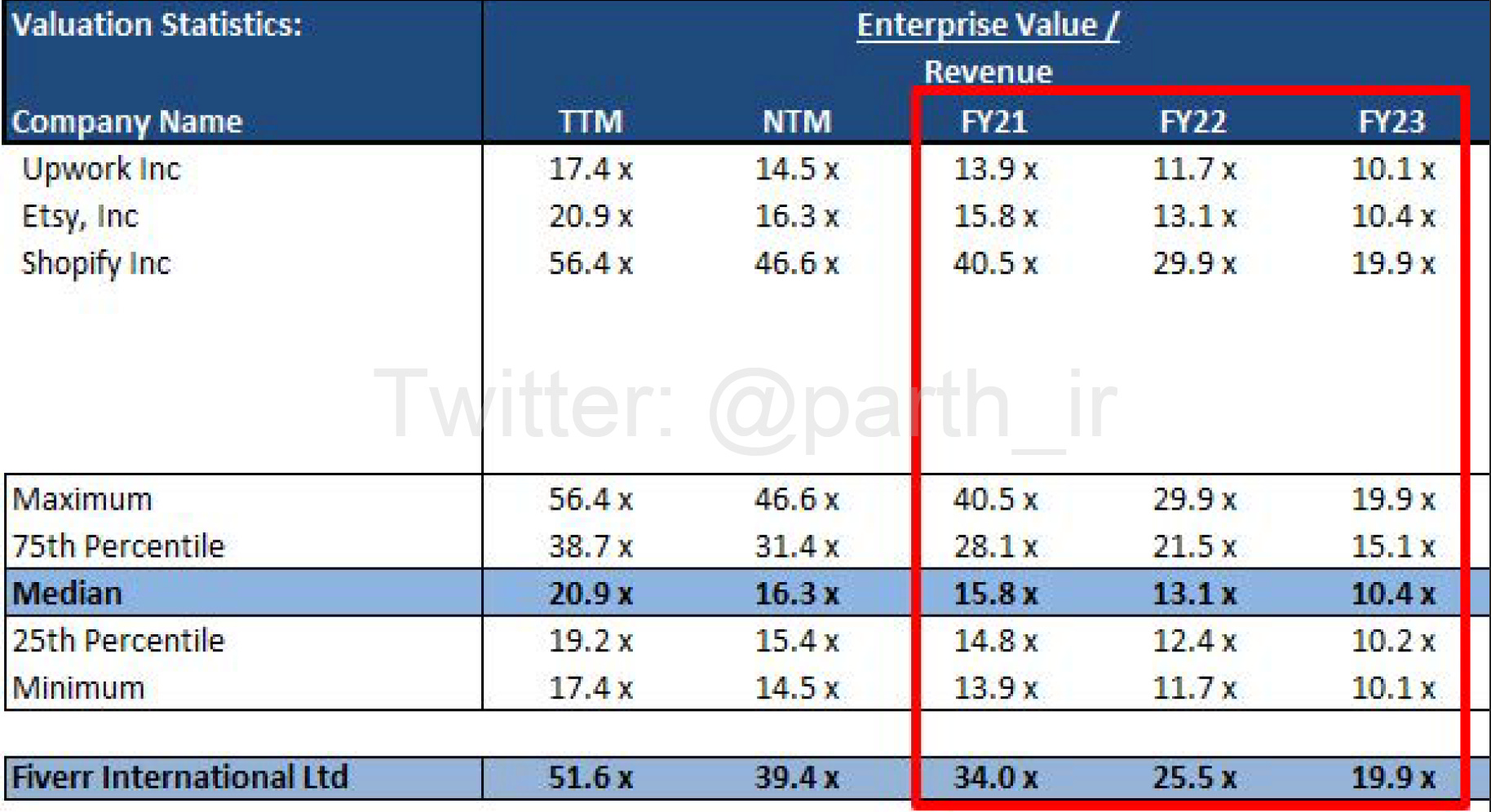

Relative Valuation

When looking at a relative valuation for Fiverr, Upwork is used as the most common comparable. However, I think Fiverr’s business more closely resembles that of Etsy or even Shopify. Fiverr provides an e-commerce marketplace for digital services as opposed to tangible products, like Etsy and Shopify. Upwork seems to be following in Fiverr’s footsteps, however, the company still resembles more of a tech-enabled staffing company than an e-commerce marketplace.

Based on these comparables, Fiverr is clearly very richly valued. I expect multiples to compress a bit going forward as Fiverr sees slower growth in FY21 compared to the pandemic-induced growth it saw in FY20.

Risks

Commoditization of gig platforms: This is the biggest risk to all gig platforms out there today. There isn’t much stopping freelancers and buyers from switching between different platforms. As I have mentioned before, the best way to mitigate this is by developing an end-to-end platform that incorporates And.Co and ClearVoice services directly into Fiverr’s platform as well as continuing to add additional services to increase platform stickiness for both buyers and freelancers. This will be especially crucial going forward as LinkedIn launches a competing platform in late 2021.

Disintermediation: This risk is inherent in the business model of any broker. Fiverr serves as the middleman for buyers and sellers. They may decide to take their relationship off Fiverr's platform. The primary way to mitigate this is to embed switching costs within their platform.

Fiverr's attempt at keeping freelancers engaged is by providing services to freelancers that help them manage their business. The main value Fiverr provides to freelancers is a marketplace to find clients. If this is disrupted with a more convenient way to provide the same service, it would be detrimental to the long-term potential of Fiverr.

Conclusion

Fiverr will continue to benefit from the tailwinds created by the pandemic and has managed to continue executing its plan to grow through international expansion, selling upmarket, and category expansion. The acquisition of WNW and SLT Consulting should continue to improve the quality of supply on the platform perpetuating the flywheel effect for Fiverr, leading to higher-quality buyers and higher spend-per-buyer. In addition to these factors, the most important thing for Fiverr to focus on going forward is embedding switching costs into their platform for both buyers and freelancers.

Valuation is stretched for Fiverr and I think it’s likely we see valuation compress in 2021 as Fiverr sees slower growth this year and faces tougher comps compared to 2020. Nevertheless, the future is bright for Fiverr and I expect to be holding my position in Fiverr for a very long time.

If you enjoyed my write-up, subscribe to stay up-to-date with my latest posts and follow me on Twitter for more frequent updates.